The Idled Engine Just Revved

Sixty years. 60% market share. And finally, an unshackled management.

I ended the last post with a tease.

A business with a near-monopoly in its niche. Serving the most demanding customers in global auto. Doesn’t advertise itself as a precision engineering firm.

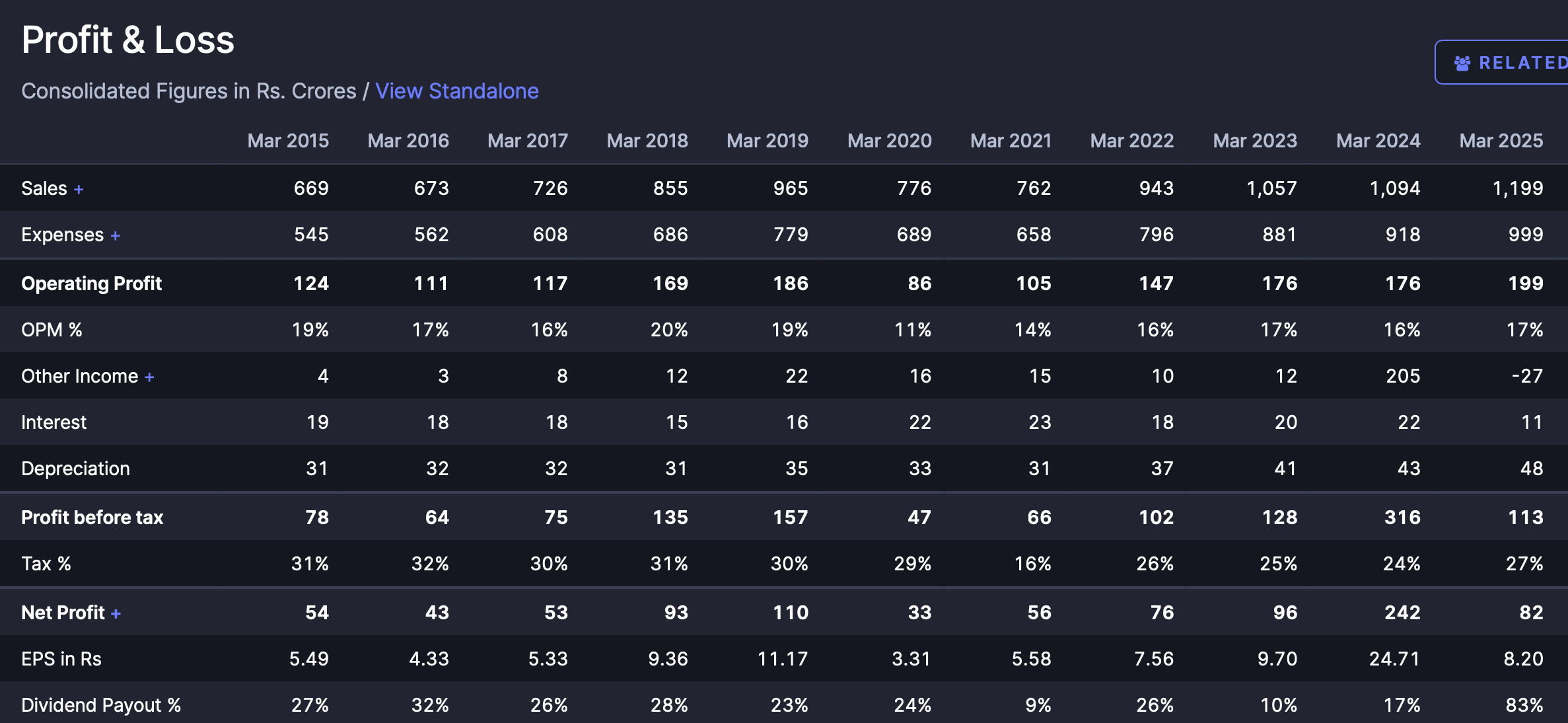

Now look at the numbers. FY15 revenue: ₹669 crore. FY25: ₹1,199 crore. That’s a 6% CAGR - barely growth. The operating margins are stable, but on the surface this screams value trap. Why bother?

The company is NRB Bearings Ltd.

NRB was the first in India to manufacture needle roller bearings - in 1965, as a joint venture with Nadella of France. Nadella invented the caged needle roller. Sixty years later, NRB holds ~75% of India’s needle bearing market and ~56% of the cylindrical roller bearing market. Over 90% of vehicles on Indian roads carry an NRB bearing.

First, a primer on what a needle roller bearing is.

Every rotating shaft in a vehicle needs to be held in place while it spins. The bearing sits between the spinning shaft and the stationary housing, carrying the load with minimum friction.

Remove the bearing, and you have metal grinding against metal at thousands of rpm. Such violent friction would seize the shaft in seconds.

A needle roller bearing solves a specific version of this problem. The “needle” is a roller with a length-to-diameter ratio of up to 10:1, think of a thin metal rod, roughly the diameter of a sewing needle, 30mm long.

This geometry packs significant load-carrying capacity into a tiny radial space. In a gearbox, every shaft is surrounded by other shafts, gears, and housings. There is almost no room. The needle bearing is what makes precision transmission design possible in that tight envelope.

A cylindrical roller bearing does a similar job but for heavier radial loads. Applications include truck axles, industrial gearboxes, and electric motors. In a 40-tonne commercial vehicle, the bearing on the axle is carrying the weight of the entire loaded truck through every pothole on every highway.

When these bearings fail, the consequences are unforgiving. A seized gearbox strands the vehicle. A failed axle bearing at highway speed can separate the wheel from the truck.

Making one needle bearing to tolerance may not be particularly hard. However, making a million of them identical (within a micron tolerance), decade after decade is something else entirely. A few microns of excess roughness can break the lubrication film. The part would fail early, and the customer cannot predict when.

This is why OEMs don’t switch suppliers lightly. The cost of the bearing is negligible relative to the vehicle. But the cost of failure and reputation is not.

Why was the growth slow?

The clearest explanation came from management themselves, on the Q3 FY26 earnings call: “We continued to be conservative and focused solely on our existing business for the past 8 years to 10 years. Starting from between 2019 to early 2025, we had performed with an entire set of structural constraints. However, we no longer face any of these constraints."

The key growth hurdle was the family friction - a prolonged disagreement between branches of the Sahney family that restricted expansion. They couldn’t align on organic or inorganic growth, so the company focused purely on defending its existing business. No meaningful capacity was added during this period.

On top of that, two operational shocks hit. First COVID. Then a fire at the Waluj plant in May 2023 that disrupted critical production lines for 18 months. This fire cost them dearly - about ₹90 crores in revenue loss.

The family settlement gave Harshbeena Zaveri (present MD and Vice Chairperson) exclusive ownership and control of the NRB Bearings and its subsidiaries.

Pulak Prasad of Nalanda Capital, in his book, counts Ms. Zaveri among best strategic thinkers in their portfolio. Nalanda has been a patient, high-conviction holder for years. Industry insiders I have spoken with echo that view.

But the real window into who runs this company opened in November 2025, when NRB held its first-ever earnings call. For a company that had spent decades being deliberately guarded, the call itself was a signal.

Ms. Zaveri declined to open with scripted remarks. Instead, she opened the floor to what she called “the questions we know are on your mind,” including the uncomfortable ones.

On the Waluj fire that destroyed critical lines, her comment is worth noting:

“We did not want to take any chance with the components that were damaged with fire. NRB chose to lose revenue rather than ship a single compromised bearing. OEMs waited. Market share came back higher.”

That call contained more about how to think about this business than any executive MBA semester.

That chapter is closed. What matters is what comes next.

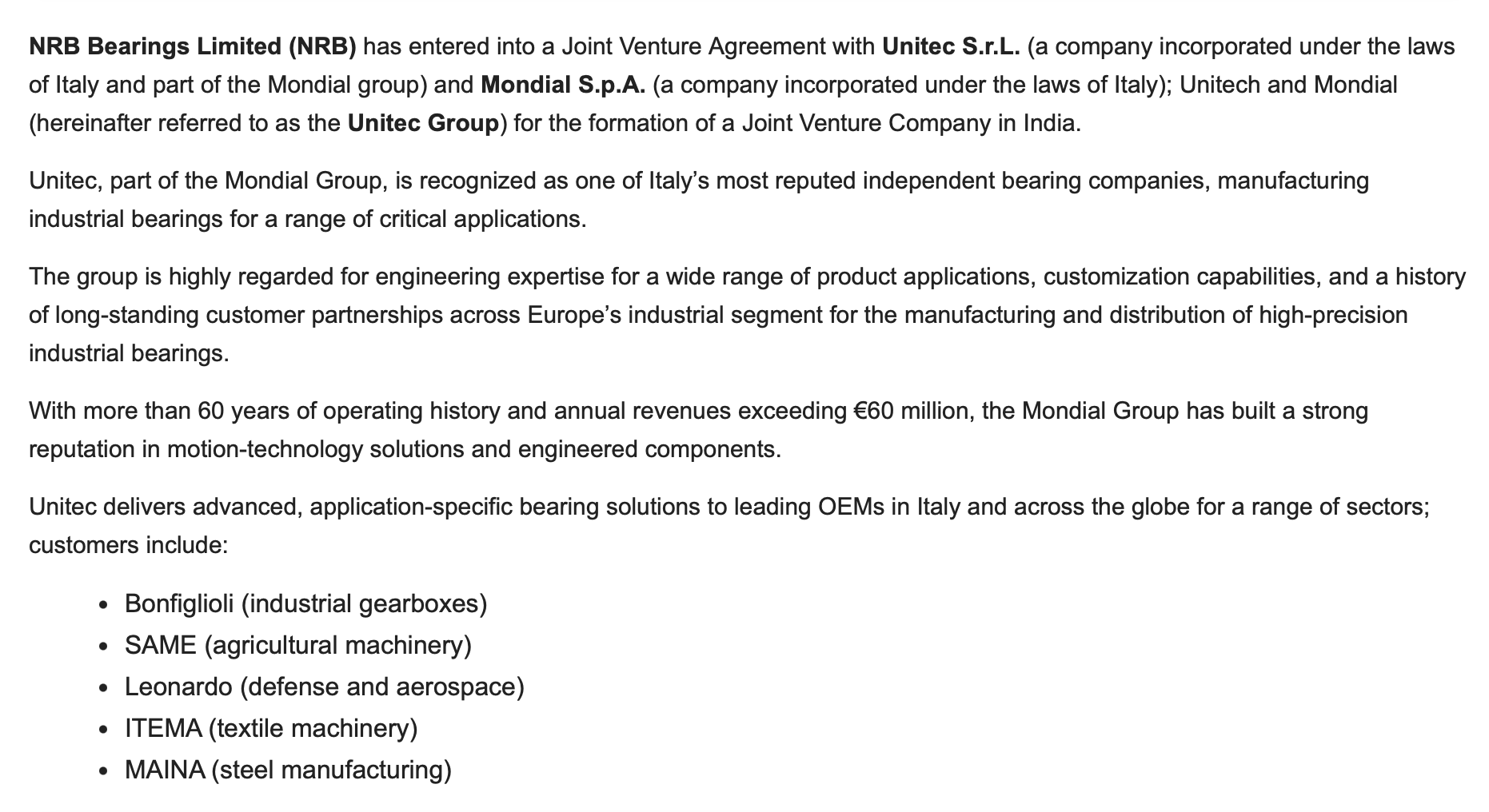

Since the settlement, the velocity of decision-making is impressive. A JV with Italy’s Unitec Group was signed in December 2025 (NRB would hold 75%). Unitec, a part of Mondial Group is a specialist in industrial cylindrical roller bearings. A LEED-certified plant is coming up in Hyderabad. The Mahant Toolroom acquisition, completed early 2026, has compressed a four-year organic aerospace journey into months.

Brownfield capacity expansion of ₹200 crore is underway - the first meaningful addition in over a decade.

The call options

The core business is known - an auto component franchise with high market share, sticky customers, and margin consistency through cycles. The call options are what makes the case interesting:

Industrial

NRB is targeting 20-25% of revenue from industrial applications over time, up from ~15% today. The segments include construction equipment, off-highway, industrial gearboxes and switchgears. These segments provided cushion against auto cyclicality. NRB joined hands with Unitec to expand into precision industrial bearings.

In the concall that happened on May 11, 2026, the management confirmed that Siemens has been added as a customer.

Aerospace

NRB had roughly ₹100 crore of RFQs from global aerospace players that it couldn’t respond to because it lacked AS9100 certification readiness. AS9100 is the baseline quality management standard for aerospace. Building that organically would have taken about four years.

So they acquired Mahant Toolroom, a proprietor run business in Bengaluru instead. As per the management, Mahant makes critical components such as landing gear parts, fuel injection systems, door assemblies for HAL platforms.

NRB paid ₹37 crore for Mahant, which came with an order book of ₹25 crore. By the May 2026 call, that order book had doubled to ₹50 crore - evidence that HAL moved faster once NRB's ownership and systems were established. NRB is expecting AS9100 certification within six months.

But the more interesting point is how NRB ended up here in the first place.

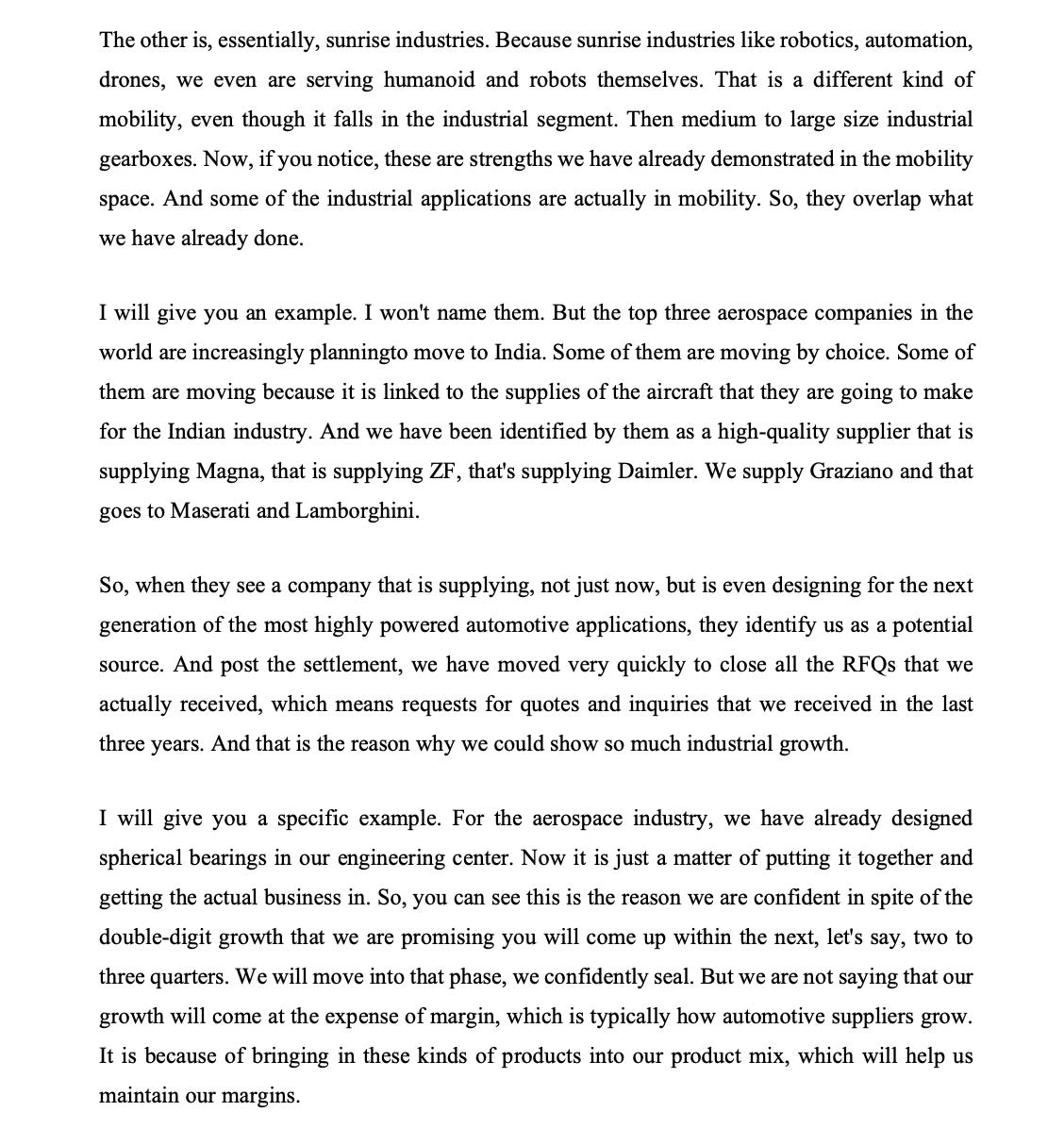

“The top three aerospace companies in the world are increasingly planning to move to India. Some of them are moving by choice. Some of them are moving because it is linked to the supplies of the aircraft that they are going to make for the Indian industry. And we have been identified by them as a high-quality supplier that is supplying Magna, that is supplying ZF, that’s supplying Daimler.” - Q3FY26 Concall, Feb ‘26

NRB is not knocking on aerospace’s door. Aerospace is knocking on theirs - because of who they already supply in automotive. The qualification logic runs backwards from what one would expect. Decades of surviving BMW and Daimler process audits has become the credential that global aerospace OEMs might be using to pre-qualify an Indian supplier.

The global aerospace RFQs that NRB couldn't touch before Mahant are now within reach.

Do give this a read: many signals in this bit of the concall

The business fits the template I highlighted in the first post: a robust automotive volume floor, industrial and aerospace optionality, and a fortress balance sheet that can fund its own transformation.

Risks

So far, this piece reads like a bullish argument. Well, not everything is perfect. The business is working capital intensive.

While inventory days have improved from 120-130 to 110; management’s target is 90-100 days. I suspect it’s achievable - if you’re pushing for growth, you invest in inventory to serve industrial customers and keep the aftermarket channels filled. High inventory is partly a feature, not a bug.

But it's also why reported PAT continues to overstate cash flows. This needs monitoring.

NRB sources some alloys from European mills with long lead times while maintaining just-in-time delivery to OEMs. That structural reality won't change overnight.

The promoter pledge, at 65.9%, is high. While the direction is right - it was above 90% at its peak, the pace would matter. High promoter pledges in India introduce a governance overhang that does not fully clear until the pledge does.

Two-wheelers make up 28% of sales. Domestic demand is showing signs of softening - Bajaj Auto recently flagged that GST benefits are being eroded by commodity-driven price hikes. The ramp may be slower than headline numbers suggest.

The FY30 revenue aspiration of ₹2,500 crore faces added uncertainty from geopolitical tensions and trade disruptions. The pattern across the last three quarters says the management delivers on its promises, though it’s early to judge.

Valuation

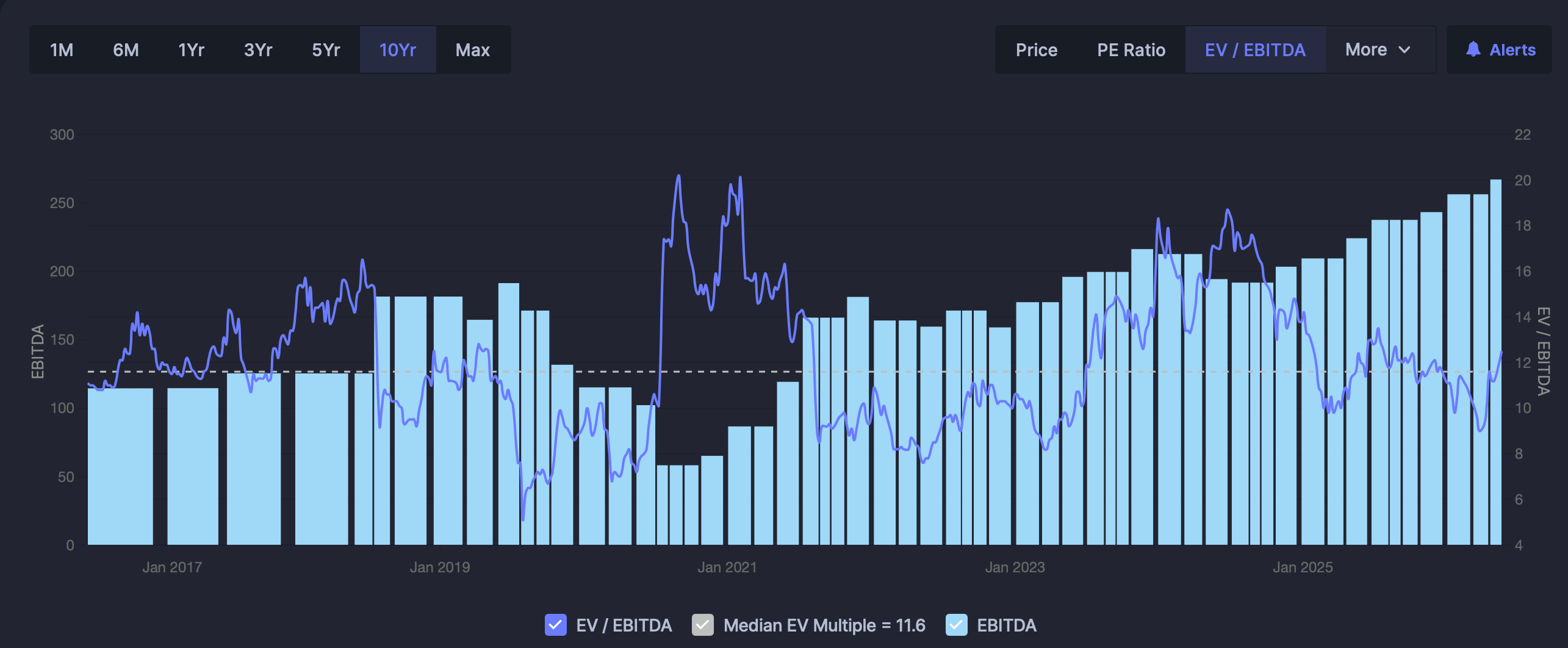

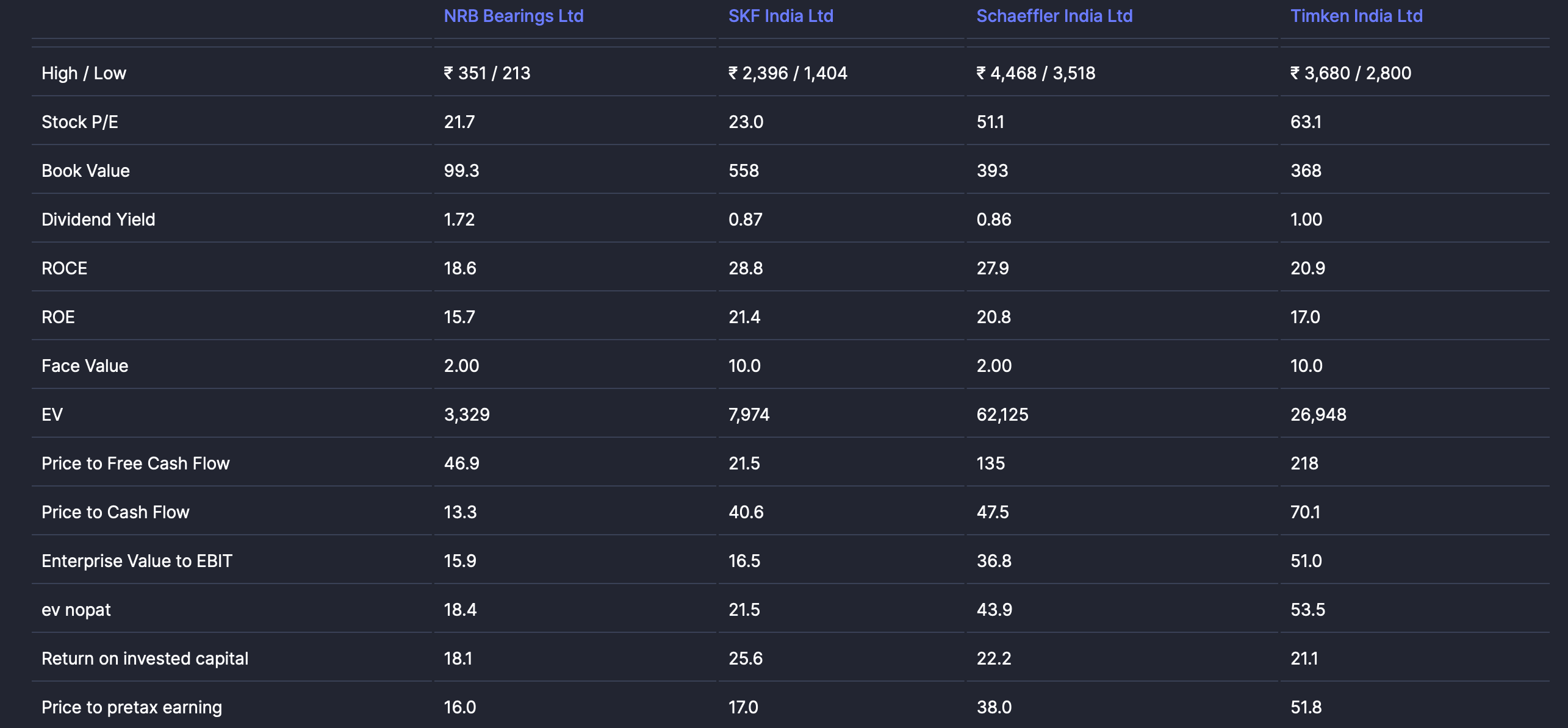

It’s not a screaming bargain. It’s valued around its 10-year median EV/EBITDA.

Cheaper than its peers (though peers are larger and have stronger portfolios). The discount exists because NRB grew slower than them for a decade. If that changes, the discount closes.

What appeals to me beyond the fortress balance sheet and the structural moat is the direction. The family settlement removed a fundamental drag that existed for years. The JV with Mondial Group and the aerospace order book give me some confidence about this company’s quality that PR wouldn’t. Albeit early, it appears that Ms. Zaveri is inclined to implement what she couldn’t earlier: invest for growth without compromising the process discipline that makes the moat real. As she put’s it:

“NRB’s focus is on businesses where the entry barriers are high. We choose the world’s most difficult customers when we enter a particular segment. Our philosophy is to get into businesses that are hard to get into because these are businesses which are hard or impossible to lose.”

As always, this is research and reflection, not investment advice. I own shares in NRB Bearings Ltd and am likely biased. Any errors in understanding are mine alone.